You don’t decide to use weather. It’s there.

That sentence is a working definition of infrastructure: data so embedded in the operational system that no one has to think about using it. It describes what weather is. It also describes what almost no commercial Earth Observation (EO) product has become.

Infrastructure is silent. Every EO sales conversation in 2026 is still an evangelism conversation. The moment you have to evangelize data, it isn’t behaving like infrastructure, even though the commercial narrative keeps calling it that.

In ‘Why Earth Observation Can’t Become Weather’, I argued that EO lacks the institutional infrastructure that turned weather into operational decision-making. This piece picks up where that one ended. The conditions for becoming infrastructure are identifiable across many domains, not just weather. Most commercial EO doesn’t meet them.

Reliability is what customers buy

What customers want is reliability. Data that’s there when they need it. The EO product market has been optimising the wrong thing for a decade. Capability is what vendors build. Reliability is what customers buy when they have a choice.

The pattern is general. People choose what removes the burden of choosing. The vendor’s job is to absorb complexity. That’s the operational definition of infrastructure: the layer that absorbs decisions so the operational layer above doesn’t have to make them. The word means the layer beneath, the part that’s there by design, invisible by design.

EO founders are selling solutions. Solutions require active decision-making at every step. Infrastructure removes decisions. The customer can feel the gap even when no one names it. They want the layer underneath; they’re being sold the trains that run on top of it.

The numbers reflect the gap. When Planet Labs went public in 2021, the company forecast that commercial revenue would grow from 54% of its total to 68% by fiscal year 2026. The actual trajectory has been flatter. Commercial mix has stayed in the high 50s through low 60s, while Defense & Intelligence has been the fastest-growing segment, expanding more than 50% year-over-year in recent quarters. The publicly listed company that bet most aggressively on commercial market formation is being pulled toward defence gravity along with the rest of the industry. The forecast was wrong about which buyer would drive growth, and the wrongness is structural.

A market structure problem, not a product problem

EO has all the visible parts of an infrastructure layer. The data exists. The dashboards exist. Some integrations exist. The operational systems that would consume satellite data automatically (insurance underwriting models, port logistics scheduling, agricultural risk pricing, supply-chain audits, infrastructure inspections) are not wired to EO the way they are wired to weather, vessel tracking, or interest rate feeds. Every EO use is still a project, a procurement, a custom integration.

The decision system exists. It just isn’t wired to the operational system it’s supposed to govern.

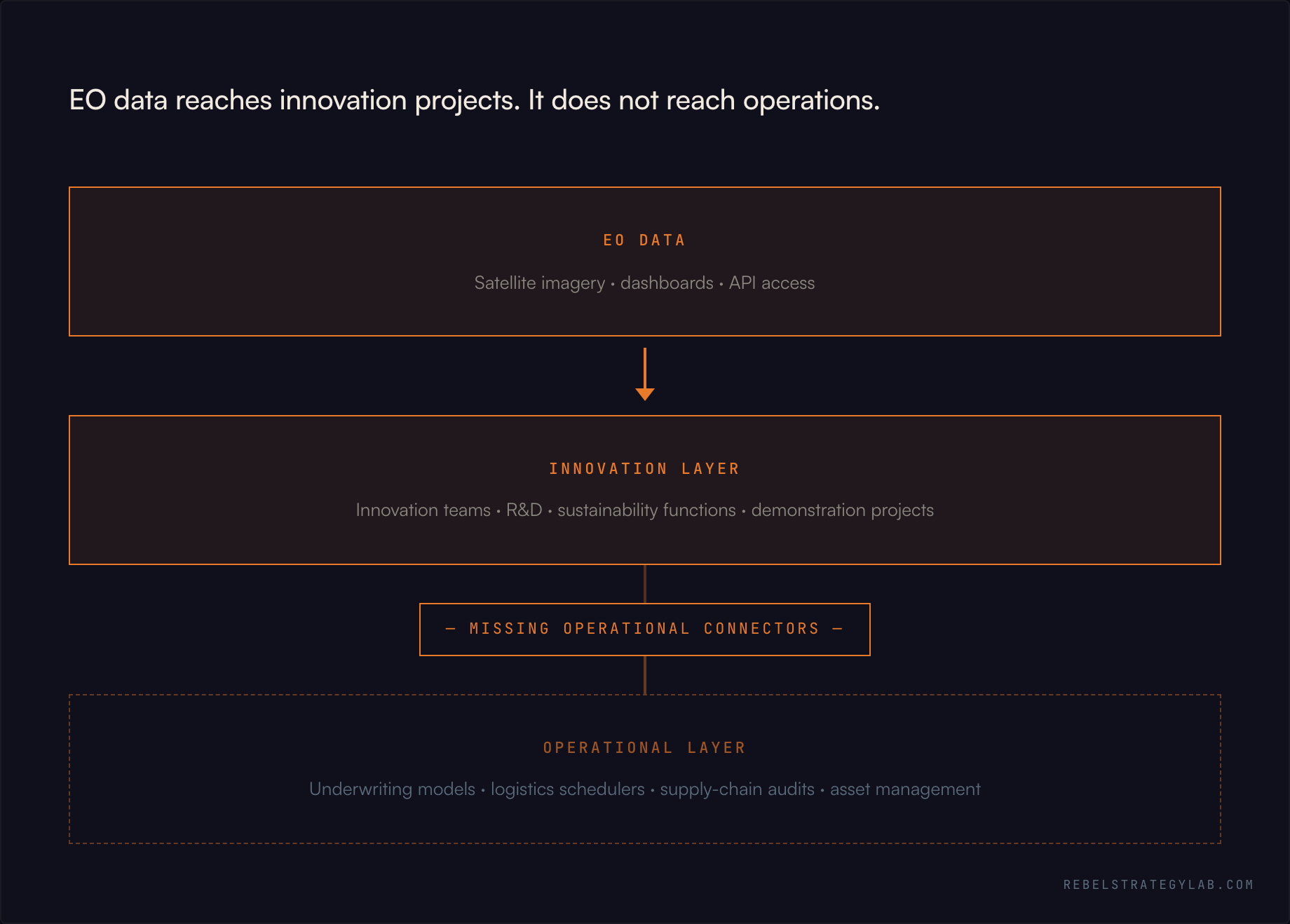

The data lives in innovation teams. Strategic-projects offices, sustainability functions, R&D groups. It almost never penetrates to the operational layer where decisions get made at the cadence of the business. The canonical version is the demonstration project that wins a press release and never reaches the underwriting desk, the trading floor, the routing system, or the asset management database.

This is a market structure problem. Better products don’t fix it because the connectors are not theirs to build.

Two reinforcing loops keep it stuck. Product loop: EO is built for technical users. That limits the buyer base. The limited buyer base keeps the product technical, because the technical buyers are who provide the feedback that shapes development. Demand loop: no operational system needs EO on a non-discretionary basis. The integrations don’t get built. Even an accessible product would have nowhere to plug in. Both loops have to break together. Founders working on either side alone, with better products or more education, cannot break them. The other loop holds the system in place.

EO data reaches innovation projects. It does not reach operations.

EO data reaches innovation projects. It does not reach operations.

Six conditions that turn data into infrastructure

Six conditions, observed across domains where the transition has happened.

1. Reliability with guaranteed availability. The data has to be there when the operational cycle needs it, at predictable cadence, without depending on weather conditions or orbit luck. If an insurance underwriter calculates premiums on Tuesday morning and the data arrives Wednesday afternoon, it isn’t operational. It’s reference material.

2. Standardisation across providers. Formats, calibration, processing chains have to be interchangeable enough that swapping providers doesn’t break the operational pipeline. Aviation weather has METAR, the standardised reporting format every airline, airport, and meteorologist reads the same way. Nothing equivalent exists for EO. Two providers’ “30-centimetre imagery” (where each pixel covers a 30-centimetre patch of ground) don’t operationally mean the same thing. Calibration, processing, and metadata differ enough across vendors that one company’s products cannot be substituted for another’s mid-pipeline.

3. Predictable, modelable economics. Pricing has to be transparent and stable enough to put in a five-year operational budget. EO is mostly project-based, custom-priced, opaque. You cannot model it the way you model cloud computing or telecoms.

4. Liability and responsibility frameworks. When the data is wrong, who carries the cost? Aviation weather has decades of case law. EO has almost none. When a parametric trigger (a pre-agreed insurance rule that pays out automatically when measurable conditions are met, like wind speed exceeding a threshold) fires falsely or fails to fire, when does the satellite data provider carry liability? Mostly unsettled. Operations teams will not run on data whose failure mode is legally undefined.

5. Operational integration. Pre-built connectors into the systems where decisions actually happen. An API is not enough. The connectors have to reach into the underwriting model, the logistics scheduler, the supply-chain audit tool, the agricultural advisory platform. The customer should not have to build the integration. If they have to, the data is being asked to behave like infrastructure while being sold like a service.

6. Non-discretionary use. The buyer cannot do the work without it. This has three sources: regulatory mandate (“you must use this”), liability exposure (“not using this creates legal cost”), or operational necessity (“the work cannot be done otherwise”). Competitive pressure converts the first two into operational necessity over time. Product strategy calls this table stakes: the baseline capability a company must have to participate in the market at all.

Conditions 1–5 are gates. Technical, economic, structural prerequisites for any data to be usable in operations. They have to be met for the data to be adoptable.

Condition 6 is the trigger. Without it, the data stays discretionary indefinitely, even when 1–5 are met. Without 1–5, the trigger fires and produces compliance theatre. The regulation arrives, the operational layer uses cheaper substitutes.

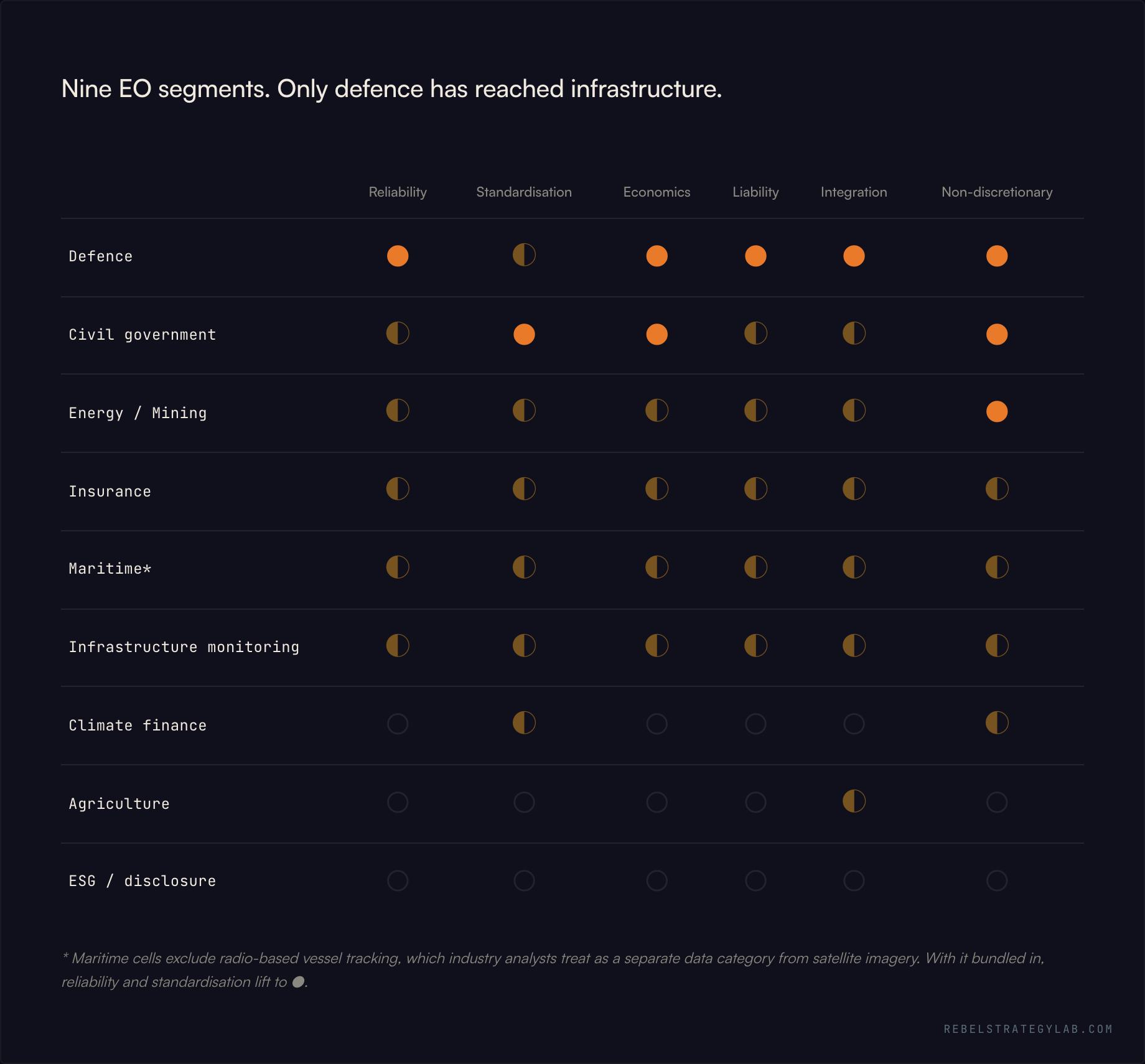

Nine EO segments. Only defence has reached infrastructure.

Nine EO segments. Only defence has reached infrastructure.

These are the obvious segments. Others follow the same logic: biodiversity monitoring, urban planning, fisheries, water-resource management. The framework is portable.

The shape that emerges:

Defence is the only fully resolved column. Operational necessity flipped condition 6 long ago, and conditions 1–5 were built privately by the buyer over decades, through procurement frameworks, military specification standards, and dedicated analytical infrastructure. The defence gravity well in commercial EO is the mechanical result of pre-regulation culture. Defence is the only segment where the data already behaves like infrastructure, and the gravitational pull on commercial EO companies looking for revenue is structural.

Civil government, when read as Copernicus plus the United States National Geospatial-Intelligence Agency (NGA) procurement, lifts to nearly fully resolved. Copernicus is the European Union’s free EO program; its Sentinel satellite series operates as managed infrastructure. The NGA’s Luno A and Luno B commercial imagery contracts ($290 million and $200 million) plus Maxar’s $359 million geospatial intelligence contract establish multi-year predictable economics on the US side. The structure differs from the commercial market in one important way: the public-good framing prevents buyer architecture from forming around payment. Civil government infrastructure exists, but it does not generate commercial market culture.

Energy, mining, and commodities is the strongest non-defence column for non-discretionary use. Two convergent forcing functions did the work. After the 2019 Brumadinho dam disaster in Brazil, the world’s largest mining companies adopted the Global Industry Standard on Tailings Management. This required satellite-based ground deformation monitoring, a technique called interferometric radar that detects millimetre-scale movement, for every facility classified Extreme or Very High Consequence. Roughly two-thirds of those facilities at companies in the International Council on Mining and Metals are now at full compliance. The EU Methane Regulation, in force since August 2024, requires the European Commission to maintain a satellite super-emitter monitoring tool with rapid-alert mechanism, including for non-EU producers selling into the EU market. The Oil and Gas Methane Partnership’s highest reporting tier, used by major operators, cannot be met without source-level satellite measurement. Tailings standards plus the EU methane regulation together convert this segment from voluntary procurement to operational requirement.

Insurance, particularly parametric and catastrophe reinsurance, is the closest commercial segment to operational status. Reinsurance market practice has hardened. Independent calculation agents have become standard in catastrophe bonds and parametric contracts; firms like Property Claim Services, part of the data analytics group Verisk, sit between the data and the payout. The 2015 dispute between Malawi and the African Risk Capacity (Africa’s pool of parametric drought insurance for governments), where a satellite-based model failed to trigger payment despite an actual drought, became the canonical convention for handling basis risk: the gap between what the parametric measurement detects and the actual loss on the ground. The buyer carries the basis risk; the modeller recalibrates. Parametric integration with insurance policy administration software is operational for the leading-edge products. The remaining bottleneck is liability framework. When a satellite-driven trigger fires wrong, the loss allocation is contractual rather than statutory, which makes scaling harder than it should be.

Maritime and logistics has structural advantages most EO segments lack. Maritime law provides a liability scaffold that aviation and shipping have settled over decades. The radio transponder data every commercial vessel broadcasts (the Automatic Identification System) is not technically EO but provides standardisation the rest of satellite data does not have. Synthetic Aperture Radar imagery, which works through clouds and at night, complements vessel tracking by detecting ships that have turned off their transponders to evade detection. These products are reaching reliability for use cases like sanctions enforcement and port-state control inspections. The International Maritime Organization (IMO) sets emissions monitoring requirements for global shipping; the EU’s Carbon Border Adjustment Mechanism does similar work for imports. Both create non-discretionary demand at the segment edges.

Infrastructure monitoring is the case where liability is the strongest cell in the matrix, which is unusual. The 2018 Camp Fire, the deadliest wildfire in California history, drove the state’s largest utility, Pacific Gas & Electric (PG&E), into bankruptcy on liability grounds. That created hard non-discretionary demand for satellite-based vegetation management around power lines. California’s Public Utilities Commission now requires it; PG&E’s expanded partnership with the satellite imagery company Planet Labs delivers weekly imagery for the entire service territory. The same pattern shows up in pipeline safety regulated by the US Pipeline and Hazardous Materials Safety Administration (PHMSA), dam safety after the 2017 Lake Oroville crisis, and urban ground-subsidence monitoring covered by international engineering standards. The liability cases are doing the work that regulation has not yet codified everywhere.

Climate finance and carbon credit verification had a real hardening event in October 2025. The Integrity Council for the Voluntary Carbon Market, the standards body that certifies the quality of carbon credits, approved a major update to the largest voluntary carbon registry’s forest carbon methodology, with explicit requirements for satellite-derived baselines. Roughly 98% of voluntary carbon market volume is now eligible for the council’s quality label across more than 30 methodologies. Under the Paris Agreement’s international carbon credit mechanism, the supervisory body adopted baseline standards in May 2025 and approved its first methodology in November 2025. Standardisation in this segment moved from absent to emerging in twelve months. Liability, economics, and integration remain weak. Companies like Pachama, Sylvera, and CTrees compete to be the satellite-data modeller-of-record for project verifications, but their integration with the registries themselves is still at pilot stage.

Agriculture is where the worked example for “integration without infrastructure” lives. The major agricultural input companies have built their satellite imagery directly into the software farmers use day to day. Climate FieldView, Bayer’s farm management platform acquired through the Climate Corporation purchase in 2013, brings satellite layers into the same software farmers use to plan planting and applications. Syngenta and Planet Labs renewed their satellite imagery partnership in 2025; Cropwise, Syngenta’s platform, opened to outside developers in November 2025. The connectors into the farm management systems farmers use are operational. Every other condition in the column stays absent. There is no service-level reliability guarantee. No standardisation across providers. Pricing fluctuates with platform strategy, not multi-year operational budgets. No liability framework for wrong prescriptions. Demand stays discretionary because conventional field scouting still works. Integration alone is not infrastructure. This is the cleanest demonstration of that fact in the matrix.

Environmental, social, and governance reporting (ESG) and corporate disclosure is where the forcing-function fragility shows up. Twelve months ago this column had emerging non-discretionary demand from three converging regulatory pushes: the EU’s Corporate Sustainability Reporting Directive (CSRD), which forced large-corporate sustainability reporting; its companion Corporate Sustainability Due Diligence Directive (CSDDD), which would have forced supply-chain due diligence on large operators; and the climate disclosure rule from the US Securities and Exchange Commission (SEC). In 2025 all three were materially weakened. The trigger has retreated. Without a trigger, conditions 1–5 do not get pulled into operationalisation. Compliance teams will use cheaper substitutes: emissions surveys, vendor self-attestation, legacy data. Satellite-derived measurement is not required, and what is not required does not get procured.

What the matrix surfaces is that “EO is going commercial” is a single narrative trying to describe nine different infrastructure trajectories. Different conditions met, different forcing functions arriving, different positions on the path. Treating EO as one market is what produces the diagnostic mismatch between the deck and the revenue.

Three paths data takes to becoming infrastructure

History gives three paths.

Operational-necessity first. The work cannot be done without the data. Defence GPS and military reconnaissance flipped to infrastructure long before any regulation arrived because the operational task (targeting, situational awareness, surveillance) could not be completed otherwise. Internet for businesses traveled the same path: by 2005 most companies could not operate without it; regulation came patchily and later, mostly around data protection, sectoral compliance, antitrust. Cloud computing has the same shape. In each case the operational layer pulled the infrastructure into existence; mandates followed.

Regulation first. Mandated use forces operationalisation, which forces standardisation, which forces integration, which forces the data to behave like infrastructure even when individual buyers would prefer it didn’t. Banking went through this through the Basel accords and central-bank reporting requirements. Aviation weather went through it through the 1944 Chicago Convention and the International Civil Aviation Organization’s standards. Aviation transponders did more recently, with the system that lets air traffic control follow every aircraft in real time. Pure regulatory paths take a decade or more even when the regulation is well-designed. Unmandated, they take indefinitely.

Tight coupling. Both forces flip together in feedback. Electricity went through this in the 1880s through 1940s, with standardisation wars between alternating and direct current, regulatory standards, liability frameworks for grid operators, and universal integration into industry and household. Cellular networks coupled spectrum regulation with commercial necessity. GPS for civilians after 2000, when the US military stopped intentionally degrading the signal, coupled commercial integration with later regulatory uses like enhanced 911 location services and automotive driver-assistance systems. Tight coupling produces the fastest infrastructure transitions. It also produces the most stable, because both forces reinforce.

EO segments are distributed across all three paths.

Defence is the worked example of operational-necessity first, fully traversed. Operational tasks could not be completed without satellite imagery. Conditions 1–5 were built privately by the buyer over decades. Procurement frameworks settled liability. The NGA’s commercial pipeline now distributes that infrastructure to other governments. The defence gravity well in commercial EO is the mechanical result of pre-regulation culture. Defence is the only segment in 2026 where the data behaves like infrastructure already, so the gravitational pull on commercial companies looking for revenue is structural.

Insurance parametric is in the early stages of the operational-necessity-first path, with regulatory tailwinds emerging. Maritime is partially regulation-first (IMO rules, port-state control, sanctions enforcement) and partially operational (dark-vessel detection where satellite radar is the only practical option). Energy, mining, and commodities is the most regulation-first commercial case in 2026, with the tailings standard and the EU Methane Regulation doing the work that operational necessity has not done on its own.

The geography of regulation matters more in 2026 than at any point in the last decade.

The EU is hardening its forcing functions for EO. The Methane Regulation entered into force in August 2024 with explicit satellite super-emitter monitoring requirements, including for non-EU producers selling into the EU. The Global Industry Standard on Tailings Management, international but EU-aligned in adoption, is converting tailings monitoring to a structural requirement. Copernicus continues to expand. Even the watered-down CSRD and CSDDD remain in force at scale levels that touch most large operators with EU exposure.

The United States is softening. The SEC voted in March 2025 to end defence of the climate disclosure rule. PHMSA’s gas pipeline leak detection rule was withdrawn under the regulatory freeze. The US Environmental Protection Agency had a methane fee called the Waste Emissions Charge; Congress repealed it in March 2025, with no collection until 2034. Agencies are pulling back from the forcing functions that would have hardened EO into US operational infrastructure.

This produces a specific structural fact for EO founders. If you optimised your product, your sales cycle, your compliance positioning for US regulatory tailwinds in 2022 or 2023, the tailwinds are gone. If you optimised for EU regulatory tailwinds, they are stronger than they were. The non-discretionary forcing functions in EO are now geographically asymmetric in a way they were not twelve months ago.

The trap underneath all of this is what pre-regulation culture rewards. Long sales cycles, custom solutions, innovation-team buyers, defence concentration. These are mechanical outcomes of a market culture where adoption is voluntary and procurement is high-friction. Optimising for those conditions makes the transition out of pre-regulation culture harder. You become better at the world you need to escape.

Why “educate the market” is the wrong instruction

The strategy being repeated everywhere in commercial EO is “educate the market.” Better content, more case studies, deeper customer research, more nuanced product positioning. The premise: if buyers understood EO better, they would buy more of it.

The premise is wrong. Markets form into infrastructure through forcing functions: regulatory mandate, liability exposure, operational necessity. Education increases sophistication of the buyer. It does not change the structure of the buying decision. Sophisticated buyers in pre-regulation culture still treat EO as discretionary. They have to. The procurement system, the budget owner, the operational layer all assume the data is optional.

Markets move into infrastructure through three actors: the regulator, the liability framework, and the operational necessity that arrives because something physical changes (climate disasters, supply chain disruption, sanctions enforcement). The founder is not on that list. Founders building products are necessary for the market to work once it forms. They are not sufficient for it to form.

The strategic question reframes. How does a company operate inside pre-regulation culture without optimising for it? The optimisation trap is mechanical. Long sales cycles teach the company to specialise in long sales cycles. Custom solutions teach the company to staff for customisation. Each of these is a local optimum that makes the transition harder when the forcing functions arrive, because the company has been built for a different market culture.

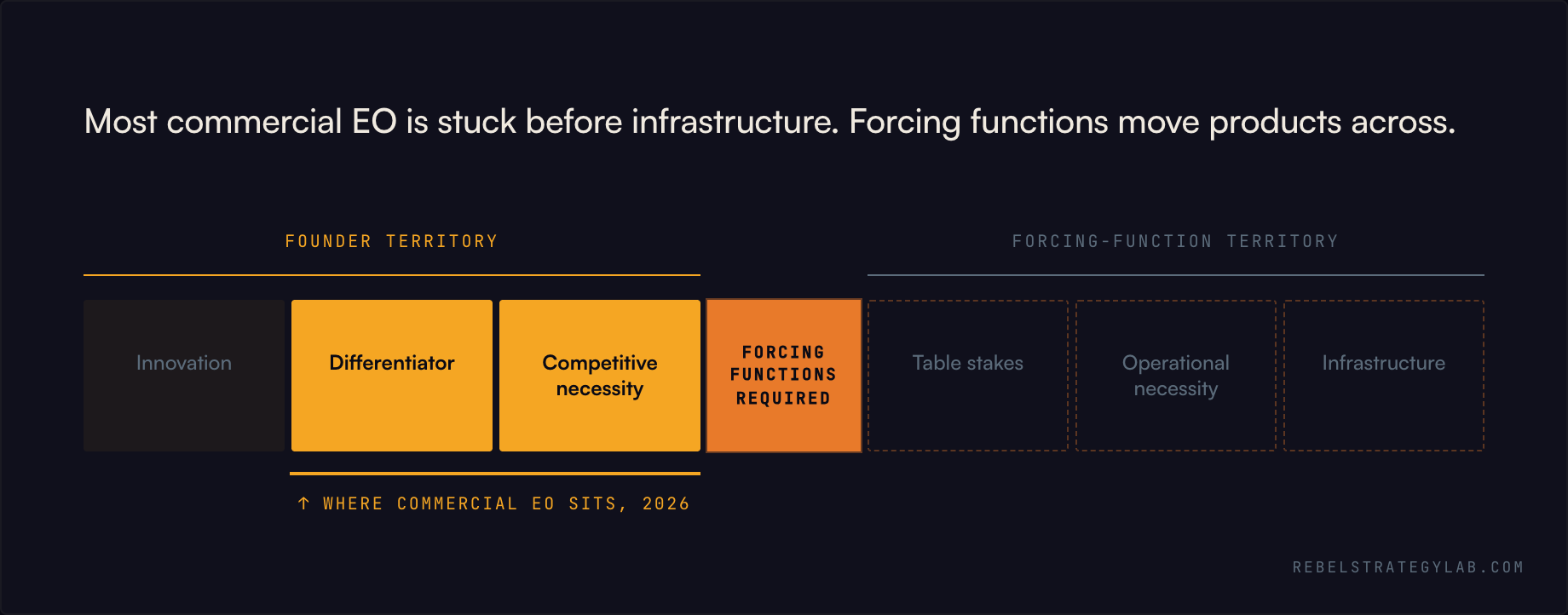

There is a useful piece of vocabulary here. Product strategy uses the term table stakes to describe a capability that has moved from differentiator to baseline expectation. It is no longer a competitive advantage. It has become required to participate. The trajectory looks like: innovation, then differentiator, then competitive necessity, then table stakes, then operational necessity, then infrastructure. Most commercial EO products are stuck between differentiator and competitive necessity, and the move to table stakes requires forcing functions the founder does not control.

Most commercial EO is stuck before infrastructure. Forcing functions move products across.

Most commercial EO is stuck before infrastructure. Forcing functions move products across.

The agriculture column in the matrix is the sharpest worked example. Climate FieldView, Syngenta and Planet, Cropwise: the connectors into the farm management software farmers use are operational. The integration condition is met. Every other condition in the column is absent. Pricing is platform-strategy-driven. Standardisation is absent. Liability is unallocated. Demand is discretionary because conventional field scouting still works. The integrated EO products in agriculture are not infrastructure. They are features inside a platform that is itself optional. Building the connector is necessary; the connector alone does not produce infrastructure. The other conditions have to land at the same time.

The fragility of forcing functions: the ESG case

Forcing functions are themselves fragile. ESG is the cleanest example. Twelve months ago, this was the segment where the regulatory tailwinds looked strongest. The EU’s CSRD was driving large-corporate sustainability reporting. Its companion CSDDD was setting up to drive supply-chain due diligence on a lookback basis. The SEC had finalised its climate disclosure rule. Three converging forcing functions across two of the largest regulatory blocs in the world.

In 2025, all three were materially weakened. The Stop-the-Clock amendment to CSDDD in April pushed the application of full obligations to 2028 and 2029 and cut scope to companies with 1,750 or more employees and 450 million euros or more in revenue. Harmonised civil liability, the lever that would have made the rule operational, was dropped. The SEC voted in March to end defence of its climate disclosure rule, after Scope 3 (the emissions accounting category covering a company’s supply chain, as opposed to its own operations) had already been removed in the final version. CSRD’s scope was cut.

The ESG segment in the matrix went from emerging non-discretionary use to absent in twelve months. Compliance teams that were planning to procure satellite-derived measurement to meet supply-chain due diligence are now planning to use vendor self-attestation, surveys, and existing emission-factor estimates. The forcing function retreated, and the operational layer did what operational layers do when they have a choice: they used the cheapest option that meets the now-weakened standard.

For founders building EO products targeting ESG and supply-chain disclosure, the lesson is hard. The forcing function you positioned around did not just slow down. It can disappear in twelve months across two regulatory blocs simultaneously. Product positioning around emerging mandates is high-leverage when the mandate hardens. It is structural exposure when the mandate softens. There is no version of this where founders can hedge by “educating the market.” The buyer’s understanding doesn’t move the system. The mandate does.

Which forcing function, by when

For founders, the strategic question reframes around a single mechanical sequence: which forcing function is arriving for my segment, on what timeline, and is my company built to be operational when it does.

The matrix shows where each segment currently sits. Energy and mining are inside an active regulatory transition the EU has converted to operational requirement. Climate finance methodologies have hardened enough in twelve months to point to standardisation completing in another eighteen. Insurance parametric is in the slow build of operational necessity through reinsurance market practice. Defence has been in steady-state for decades.

For other segments the picture is harder. ESG just demonstrated that forcing functions can retreat as fast as they arrive. Agriculture has integration without a forcing function in sight. Civil government beyond Copernicus and the NGA is divided by national procurement maturity. Maritime is half-coupled, narrow use cases.

This question is mechanical. It depends on jurisdictions, physical reality, political cycles. None of those are inside the founder’s control. That is what makes it harder than “educate the market.” It is also closer to how commercial EO becomes commercial. The market does not form when products improve. It forms when forcing functions arrive at conditions that are already met.

Anyone betting a company on “educate the market” in 2026 is betting on the variable that doesn’t move the system.